Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Pensacola’s housing market is heating up again

And it still has the most competitive prices and the best white sand beaches in Florida

Let’s chat about

To all my wonderful clients ,

I extend warm greetings on the special occasions of Father’s Day to have a

wonderful day with your dad and kids!

By

“In the midst of a “housing recession,” homebuilders say they see signs of a turnaround on the horizon.

New-home construction continued to be constrained in February as the costs of building materials remained high. At the same time, rising mortgage rates and new economic fears about the banking sector are shrinking the pool of potential buyers. Yet home builders are feeling upbeat.

Builder confidence in newly built single-family homes rose for the third consecutive month in March, according to the National Association of Home Builders and Wells Fargo Housing Market Index. Builders say they believe a lack of existing housing inventory will shift homebuyer demand to the new-home market. “A significant amount of housing demand exists on the sidelines,” says NAHB Chairperson Alicia Huey. “Even as builders continue to deal with stubbornly high construction costs and material supply chain disruptions, they report strong pent-up demand as buyers wait for interest rates to drop.”

Last month, single-family home construction posted a modest 1.1% gain on a seasonally adjusted annual basis. But construction is down nearly 32% compared to a year ago, the Department of Housing and Urban Development and the Census Bureau reported Thursday. Builders have tapped the brakes amid surging mortgage rates, which are nearly double what they were a year ago.

However, rising builder confidence signals a potentially sharper turning point for home building later this year, says NAHB Chief Economist Robert Dietz. “We expect volatility in the months ahead as ongoing challenges related to construction material costs and availability continue to act as headwinds on the housing sector,” he says. “However, interest rates are expected to stabilize and move lower in the coming months, and this should lead to a sustained rebound for single-family starts in the latter part of 2023.”

But the latest wild card: jitters over the nation’s financial system after the recent collapse of three banks. But that could reduce long-term interest rates, which “will help housing demand in the coming weeks,” Dietz says. “The cost and availability of housing inventory remains a critical constraint for prospective home buyers.”

Only 830,000 single-family units were started in February, which is well below the historical average of 1 million units—a threshold often cited to meet population growth. “It is understandable, given high mortgage rates, for home builders to be cautious,” Yun says. “However, once rents and consumer price inflation calm down, mortgage rates will be lower.” Though that will likely bring more buyers to the market, it remains to be seen whether there will be enough inventory to satisfy demand, he adds.

Existing inventory remained low in January at a 2.9-month supply but has inched up by 15.3% compared to a year ago, according to NAR data.

Home builders are trying to get buyers’ attention: Thirty-one percent say they reduced their prices in March, while 58% say they provided some type of incentive, such as a mortgage rate buydown, according to NAHB data. The trade group attributes the increase in new-home sales over the last two months to the increased use of incentives and price discounts.

Meanwhile, multifamily starts are a notable bright spot for the new-home sector, climbing 24% in February to an annualized 620,000-unit pace, HUD and the Census Bureau report. More is on the way, too: Multifamily permits in February rose 21% on an annualized basis.

“The market is responding to solid rent growth and low vacancy rates of both apartments and single-family rental units. But with such active construction, plenty of empty units will be hitting the market throughout this year and next,” Yun says. “Rents will calm down and even drive the overall consumer price inflation to be manageable.”

“Shelter” makes up one of the largest components of the Consumer Price Index, which largely is measured by rent costs, and has been cited as a significant contributor to sky-high inflation in recent months.”

https://www.nar.realtor/magazine/real-estate-news/builders-are-upbeat-in-the-face-of-market-headwinds

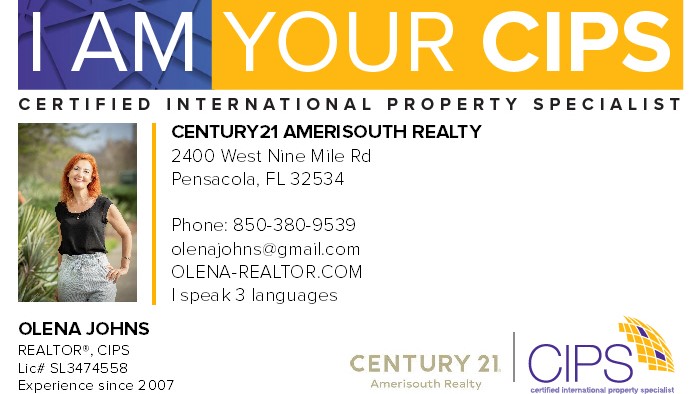

What is a CIPS?

A Certified International Property Specialist (CIPS) is a global real estate professional who has undergone specialized training to complete international transactions seamlessly and with reduced risk. The CIPS designation is the only international designation recognized by the National Association of REALTORS®.

Only REALTORS® who have completed extensive coursework and demonstrated considerable experience in international business are awarded this prestigious designation.

Value Proposition

As a Certified International Property Specialist,

I have the training, resources and experience to help you purchase property in the United States. I have worked with buyers from locations around the world, and I can help you understand the process. With access to the CIPS global network and REALTOR® technology, I can help you find and purchase the property that is right for you.

My goal is to streamline and simplify the process of buying real estate in the United States. My services can save you time and money. Just give me a call !

Olena Johns +18503809539

#InternationalRealtor #Floridarealtor

The Florida program is distinctive in that it is broader than the federal program, because it regulates the alteration of uplands that may affect surface water flows and “isolated” wetlands falling outside of federal jurisdiction. Florida regulates all land disturbance that could have an effect on state waters, whether or not the activity itself occurs in state waters. From a sea level rise adaptation perspective, this kind of scope could enable Florida to provide protection to dry, potentially inundatal lands, although there is no indication that they are doing so now.

https://www.floridarealtors.org/news-media/news-articles/2023/05/wetlands-oversight-still-confusing-after-court-decision?utm_campaign=6-1-23+Florida+Realtors+News&utm_medium=email&utm_source=iPost

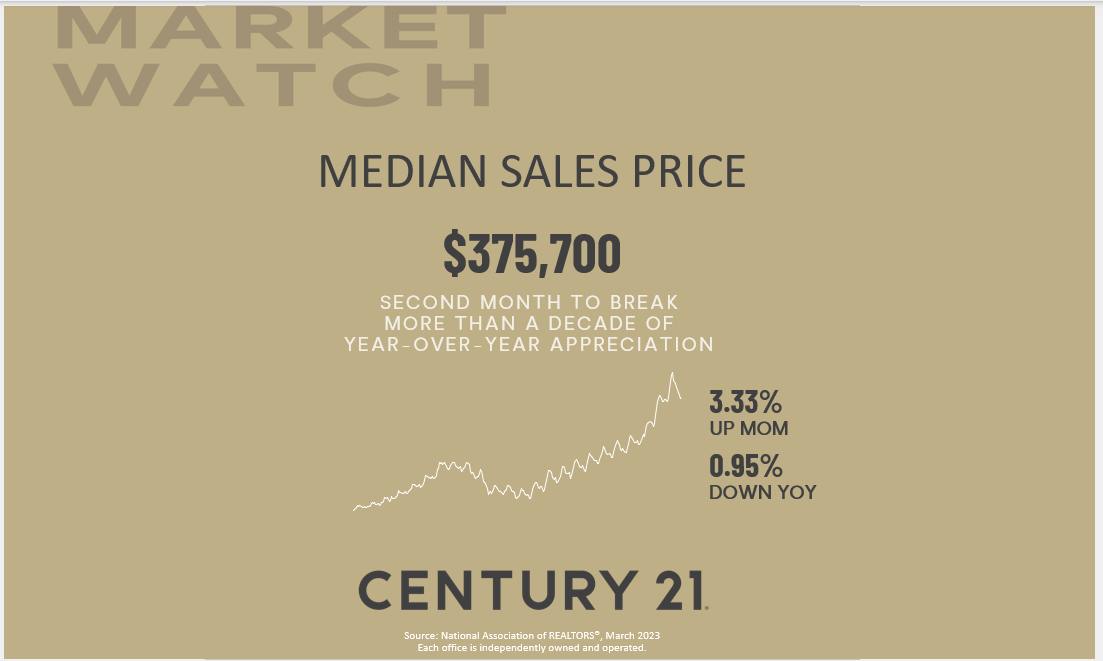

Pensacola , FL housing market update is well in line with the national housing forecast.

According to

Median sales prices is going up compared with the last year .

While the seasonally adjusted rate declined from February to March ( by national stats) , the actual ram number of homes sold increased by 34%.Buyers are taking advantaging of interest rate between 6.3-6.4%

Message/call me if you are considering your options- we’ll run the numbers and see what your property is worth!

Olena-realtor.com

#olenajohns #internationalrealtor #housingmarketexpert #salesexperts #floridarealtor #century21agent #property

10 Financing Options to Consider

As the market evolves, it’s vital to know some of the lesser-used financing options. Be sure to ask your real estate agent or mortgage professional about these when you get pre-approved for home financing.

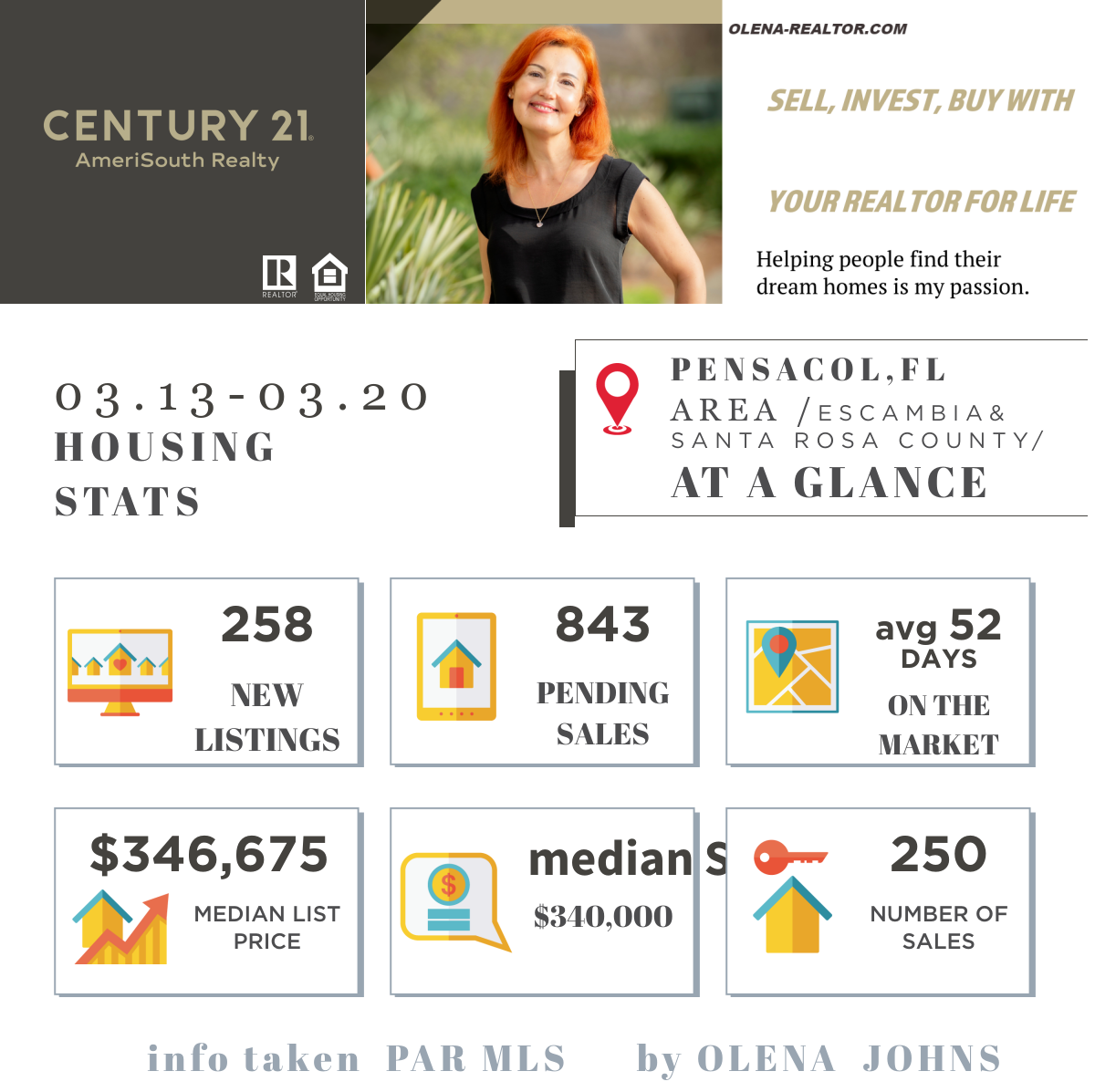

Of course in compare with last year (by Pensacola Association of Realtors data)

Closed Sales decreased by 16% ,

though inventory increased by 154%, which should be of interest to out-of-state

buyers who are still looking to invest their money in Florida real estate.

And the median Sales Price increased by 1.6% compared to last year, which was

pretty good for the Pensacola area.

Developers continue to build new communities and Pensacola becomes more attractive

not only due to the white sand beaches and Southern traditions, but because

of affordable real estate prices. So if you’re thinking about it, let’s just chat

#olenajohns #internationalrealtor #риэлтор

#флорида #недвижимость #realtor #флорида

#риэлтор #floridarealtor #olenajohns #century21agent

https://youtube.com/shorts/R-gAEFQLF6E?feature=share

Your REALTOR for Life

According Internal Revenue Services, National Association of Realtors, U.S. Department of State,

Buying real estate in the U.S. is different than in many parts of the world. Here are 8 questions to answer before you sign a contract for the perfect Florida vacation home.

In the U.S., all Realtors list properties in the Multiple Listing Service (MLS). All agents can show any property found online.

The process from having an offer accepted to closing on the home takes about 30 days but may take longer if you need to secure financing.

You may purchase the property as an individual or through a legal entity, such as a limited liability corporation (LLC). If you choose an LLC, it could protect the property from estate and gift taxes and limit liability should an accident occur; but every situation is different. Consult a tax attorney who specializes in international transactions before making a final decision.

Do you plan to obtain a mortgage or pay cash? You may find that U.S. lenders charge foreign buyers a higher interest rate than they do U.S. buyers. You may also have to put down a downpayment of 30% or more of the purchase price.

In addition to the purchase price, buyers of U.S. properties face costs such as title search and insurance and recording fees that can add between 1.5% to 3% to the final cost of the home.

The amount of time you can stay in the U.S. varies by your country of origin. Residents of select countries, including Canada, do not need visas to visit the U.S. For more information, go to travel.state.gov

Possibly. Many countries offer the ability to do closings through remote online notarization. Consult your title company for your options.

Real estate agents can do a lot more than find you a property and help you with the offer and contract. Many specialize in working with global buyers. Often these agents have a team of experts including tax attorneys, international lawyers and international accountants, who can smooth the process of buying and owning a home in the U.S.

Happy St Patrick’s Day !

I hope you can get some magic shamrock 🍀and meet a leprechaun 🧝who will find a piece of gold for your HOUSE 🤗

All you need is love and chocolate.

Wherever – and with whomever – you’re spending Valentine’s Day,

we hope you have a lovely day !

Sincerely,

Olena #yourREALTORforLIFE

According Floridarealtors.org/ by Brad O’Connor/

“In December of 2021, the average 30 year fixed mortgage rate in the US was about 3.1%. Based on data published by Freddie Mac. And that, by the way, was the highest monthly average rate we had seen since June of 2020.

Fast forward just 12 months to December of 2022 and the U.S. housing market was facing an average 30 year fixed mortgage rate of nearly 6.4%. The impact of that kind of change can’t be overstated. Let’s consider a 30 year fixed rate loan on a $300,000 home with 20% down.

At a rate of 3.1%. The monthly principal and interest payment on that mortgage would be $1,025. But at 6.4%, that’s a 1500 dollar monthly payment, a nearly 50% increase. It should come as no surprise then that we had significantly fewer homes going under contract in December 2022 than a year ago, in December 2021. According to the latest statistics from Florida Realtors. New pending sales of single family homes were down 31 and a half percent year over year in December. One of the only silver linings here is that this was actually an improvement over the year over year declines of 41 and 37% reported for October and November, when rates were at higher average levels of about 6.9 and 6.8%, respectively. There is increasing consensus among economists that inflation has likely peaked and as a result, mortgage rates have topped out as well. Should this prove to be true, there will still be a big question looming over the housing market here in Florida and the rest of the US, which is how slowly and how much will mortgage rates recede from here? Unfortunately, there’s no easy answer to that. Interest rates are notoriously difficult to forecast. Even in normal times when the Federal Reserve is not actively shifting its monetary policy to this degree.”

HOWEVER Rent price for the same $300,000 house price in Pensacola/Panhandle area may exceed $2,000 which shows the buying expediency today with other homeownership advantages .

More info about Pensacola, FL housing market you can find bellow

or call me/Olena Johns 850.380.9539

Your Realtor for Life

For most of us, our bedroom is little more than a place to sleep and relax. However, just because it’s always been that way doesn’t mean that we have to settle for drab and dreary.

One trend that’s gaining steam these days is converting your current bedroom into a luxury suite (or something comparable). If you want to live like you’re renting a room at the Ritz, then you want to follow these tips.

Compartmentalize Your Activities

Making your bedroom more functional is going to make it more luxurious. Add a gorgeous desk for working and a TV area for entertainment, and you’ll be living it up in no time.

Make it Chic

Choose a color palette that is both luxurious and classy. Silver and gold can seem tacky, so choose muted shades that compliment each other.

Also, a brilliant and commanding headboard can instantly upgrade the look of your room without any other changes.

Light it Properly

Finally, make sure that you have the right light to show off your designs. If it’s too washed out or yellow, then it will look drab and run down. Switch to brilliant LEDs and see the difference.

Choose Your Accents Wisely

We already mentioned a headboard, but some elegant drapes can also make your room feel more royal. Being strategic with your furniture accessories is going to both keep you under budget and avoid doing too much with the space.

Are you ready to lux your bedroom? You’ll be impressed by the results, and the feeling of decadence will make you more confident in your surroundings.

© 2026 MoxiWorks

© CENTURY 21 2023 - 2024. All rights reserved. CENTURY 21®, C21® and the CENTURY 21 Logo are registered service marks owned by Century 21 Real Estate LLC. Franchisee Legal Entity Name (not the dba) fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each franchise is independently owned and operated. Any services or products provided by independently owned and operated franchisees are not provided by, affiliated with, or related to Century 21 Real Estate LLC nor any of its affiliated companies.